Updated May 2026

What Is Liability-Only Auto Insurance Insurance?

Liability-only auto insurance is the minimum coverage required in nearly every state. It pays for injuries and property damage you cause to others in an at-fault accident, up to your policy limits. It does not cover damage to your own vehicle, your medical bills, or repairs after a single-car accident. For drivers reinstating after a suspension for unpaid tickets or fines, liability-only meets state reinstatement requirements at the lowest cost.

- You rear-end a car at a stoplight. The other driver has $8,000 in vehicle damage and $15,000 in medical bills. Your liability coverage pays both, up to your policy limits. If you carry 25/50/25 limits, the property damage is covered in full and the medical claim is covered up to $25,000 per person. Your own vehicle damage is not covered—you pay that repair bill yourself.

- You sideswipe a parked car, causing $3,500 in damage. Your liability coverage pays for the parked car's repairs. Your vehicle sustains $2,200 in damage. Liability does not cover your own vehicle—you pay the $2,200 out of pocket or file a collision claim if you carry that coverage.

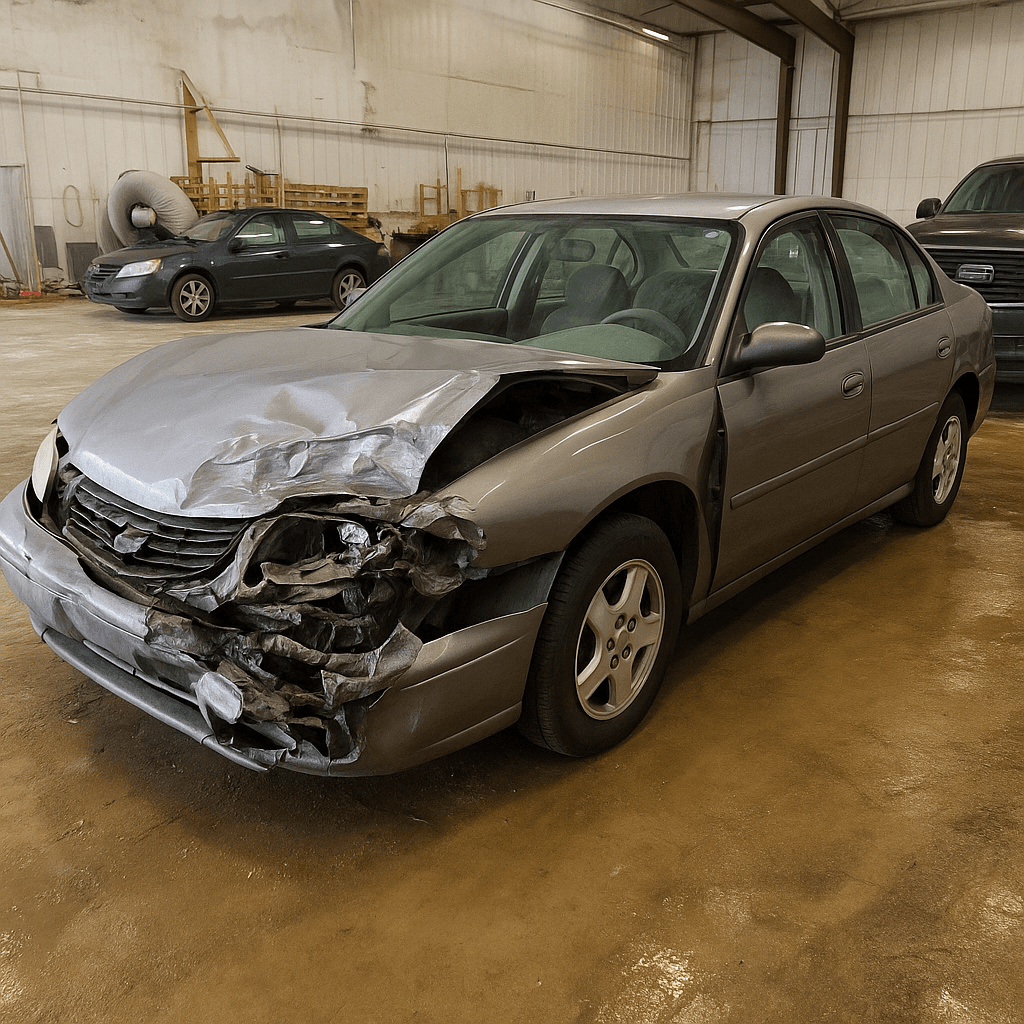

- You lose control on a wet road and hit a tree. Your vehicle has $6,000 in damage. Liability-only pays nothing because no other party was injured or damaged. You cover the entire $6,000 repair cost yourself. This is the most common scenario where drivers with liability-only realize the coverage gap.

How Much Does Liability-Only Auto Insurance Insurance Cost?

Liability-only costs $40–$90 per month, or $480–$1,080 annually, for drivers reinstating after a fines-based suspension.

- State minimum liability limits—higher minimums in states like Alaska ($50,000 per person) cost more than lower minimums in states like California ($15,000 per person).

- Driving record—prior at-fault accidents or moving violations increase liability premiums by 20–40 percent, even without a DUI.

- Zip code—urban areas with higher accident rates and repair costs increase liability premiums compared to rural counties.

- Credit history—in states where credit-based insurance scoring is allowed, lower credit scores increase liability-only premiums by 30–60 percent.

- Coverage limits chosen—selecting 50/100/50 limits instead of state minimums increases premiums by $15–$35 per month.

- Prior suspension length—a suspension lasting over six months signals higher risk to carriers and increases premiums by 10–20 percent.

See How Much You Could Save

Get personalized liability-only auto insurance insurance quotes in minutes.

Who Needs Liability-Only Auto Insurance Insurance?

Liability-only is recommended for drivers reinstating after a fines-based suspension who own older vehicles worth under $3,000, drive infrequently, or cannot afford comprehensive and collision premiums. It satisfies state reinstatement requirements at the lowest legal cost. If your vehicle is paid off and worth less than $2,500, the cost of collision and comprehensive coverage often exceeds the payout you'd receive after a total loss.

If your vehicle is worth less than $3,000 and you have $3,000 in savings, liability-only makes financial sense—you can replace the car yourself if needed. If your vehicle is worth over $5,000 and you have no emergency fund, the risk of total loss after an at-fault accident outweighs the $30–$50 per month you'd save by dropping collision coverage.